Outlook 2009: Whats left to say?

If you did nothing but watch cable news or read op-ed pages, probably you’d have as much insight to the 2009 economic outlook as economic researchers and financial experts. Since the collapse of global financial markets in September — a collapse preceded by a year or more of weakening economic conditions due to rising energy and commodity costs and increasing capital costs — there is complete agreement: things have never been worse.

So, it’s not especially revealing when reliable market forecasters predict more trouble ahead. The Deloitte & Touche expert for manufacturing and industrial products markets, Tim Hanley, delivers a typical example:

• Manufacturers are enduring falling share prices and weakening valuations.

• Their supply chains are “increasingly vulnerable” because of limited credit availability and economic decline in general.

• Costs of commodities and energy are becoming more unpredictable and unstable.

• Increased competition and weakened global demand are limiting manufacturers’ ability to pass on costs to consumers.

• Difficult-to-obtain financing amid a tightened credit market is inhibiting expansion planning.

• Investors, consumers, and regulators are forcing the concept of “sustainability” into the manufacturing agenda. And,

• A shrinking domestic “talent pool” of capable managers, executives, and engineers, combining with an aging workforce and global recruitment and retention problems, poses a significant barrier to industrial growth.

Expert insights have to be credited with some understanding of what’s going on in the manufacturing sector, but there’s not much not there that can’t be concluded from the headlines. Or, even from experience.

But, if one is going to make 2009 plans based on gloomy forecasts, it might be wise to look for more specific details. The Foundry Management & Technology 2009 Business Outlook Survey covers many of the same concerns as the Deloitte tipsheet, but the conclusions are less clear. In some cases they’re even reassuring, or encouraging.

Number crunching

First, let’s set the facts: FM&T surveyed the leading managers and executives of all the North American metalcasting plant locations in our circulation — roughly 2,100 sites. The survey was conducted in October 2008, coinciding with the period of time now understood to have been the first wave of financial panic, following 15 months of weak industrial activity (see the results of our 2008 Business Outlook Survey in the December 2007 issue), and several years of heightened awareness about the various threats the analyst cites: commodity prices, energy costs, borrowing difficulties, training and staffing, and environmental compliance.

The timing of our survey was certainly significant. The level of response, while still credible, was down notably from the survey we conducted in 2007. Seemingly, frustration and distraction among our addressees discouraged responses. It certainly discouraged some who did respond — including the two managers at a well-known ferrous foundry who returned the unanswered survey in the form of confetti.

As summarized by one responding manager at a small, specialty operation: “I believe the foundry industry will see a poor business climate until the banking/investment fiasco and media dramatization of that fiasco cools and moves on to some other ‘crisis’.”

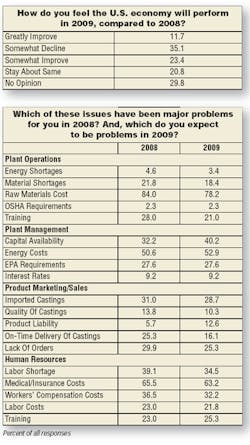

But, now, look at the results. In the most wide-open inquiry — “How do you feel the U.S. economy will perform in 2009, compared with 2008?” — a plurality (35.1%) of respondents feel there will be a decline. That figure, though, is less than the percentage (38%) who anticipated (correctly, it turned out) a decline during 2008. More revealing, is that the percentage of this year’s respondents who feel the economy will improve “greatly” (11.7%) or “somewhat” (23.4%) is equal to the number that anticipate a decline. The remaining respondents who decline to offer an opinion on this subject may be the most insightful.

There must be a point, however, at which the atmosphere of gloom overtakes reasoned insight. For example, asked to list all the problematic issues for their metalcasting operations, most respondents identified raw material and energy costs. This is understandable: each of those issues is well covered by news, and well understood from expense reports and individual experience. Both were likewise among the leading problems identified by readers for 2008.

The next leading area of respondents’ concerns about 2009 involves the availability of capital. Again, this is a well-reported and -understood issue, and the results may reflect individual experience, too.

But, the problem areas that follow this in our respondents’ estimation are not new concerns, nor ones that are likely to be magnified by changing economics. Indeed, they are problems that were almost equally concerning in 2008: insurance costs, labor shortages, imports, and so on.

The particular, longstanding concern about metalcasting imports provides an interesting example. A plurality of our respondents (41.4%) agree that imports are a threat to their success, but then a majority do not. In fact, 32% of our respondents see no affect on their business from imported castings, while 17.2% see the threat as diminishing. This effect has been emerging in the year or so since the U.S. dollar began declining in value versus major world currencies — which created a circumstance in which some metalcasters could reverse the effect on their business by increasing exports (9.2%)

Of course, falling currency rates create a new range of problems that affect everyone banking on the U.S. dollar. “Imports are not the biggest threat to our business,” one manager of a mid-sized iron foundry commented. “The U.S. government is by far the biggest threat to our business, and our way of life.”

Thoughts and actions

Now, how will our respondents apply their 2009 business outlook, in practical terms? We tailored our survey to find out the borrowing and investment plans of metalcasters during the coming year. In terms of actual dollars they plan to spend, our respondents do not appear to be holding back as a result of any actual or perceived problems.

As of October, budgets remain in place for some considerable capital spending by metalcasters in 2009. Ferrous metal operations — gray and ductile iron, steel — have the highest-value projects reported to us, including several in the multi-million dollar range. Aluminum casting projects are not without mention, either.

The overwhelming number (71.2%) of these projects involve new equipment, however, only 12.2% call for any plant expansion. We discovered no 2009 plans for new plant construction.

In terms of the purchasing plans there is no clear direction among our respondents, though it’s possible to draw at least one conclusion: Money marked for 2009 investments is focused on improving plant productivity.

The most commonly identified purchase in the coming year will be pollution controls, a catch-all term that may refer to baghouse systems, scrubbers, or any number of other systems. The world at large sees such technology as an effort to “clean up” an operation; metalcasters know that pollution controls are a way to reduce the regulatory burden that prevents an operation or an organization from achieving its full potential of performance and productivity.

The next most commonly listed purchase plan identified by our respondents involves melting equipment. Again, the reading of this is a nod toward greater productivity, with new furnaces that melt faster, or cleaner, or produce higher volumes of metal, or do so with greater efficiency.

Following in popularity are a series of planned purchases that will lead to greater plant productivity. New grinding machinery, shakeout/punchout equipment, and blast cleaning systems should lead to cleaner castings, and likely to higher volumes, too. New conveyor systems should allow more efficient and/or higher volume production processes.

There is no clear message in the 2009 Business Outlook Survey, but in the prevailing atmosphere a “clear message” may be too much to expect.

However, there is a message of determination. “Business is good,” one steel foundryman wrote to us, “but we are always looking for ways to improve. We are currently looking at ways to increase our size range, and to offer a wider variety of services, starting in the design phase all the way through the machining phase.” That’s the sort of attitude one has to assume in order to manage through the confusion.

About the Author

Robert Brooks

Content Director

Robert Brooks has been a business-to-business reporter, writer, editor, and columnist for more than 20 years, specializing in the primary metal and basic manufacturing industries. His work has covered a wide range of topics, including process technology, resource development, material selection, product design, workforce development, and industrial market strategies, among others.