Metalcasting Business Outlook 2015: Present Results, Future Prospects

Foundry Management & Technology readers are in general agreement with the expert economic analysts. Each year, during September and October, FM&T surveys metalcasters to measure the outlook of men and women working in North America’s foundries and diecasting plants. We seek to identify the problems they face in their businesses and the economy, to learn what plans they're making for the coming business cycle, and to understand better they're expectations are for the year ahead.

This is the second article of a series. Read Part 1, Metalcasting Business Outlook 2015

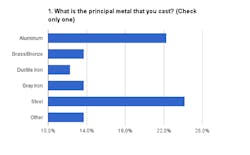

We surveyed readers by email over a period of six weeks. The results include responses from over 200 readers, executives and managers whose operations produce a representative range — see Chart No. 1 — of cast metals: aluminum (22.3%), brass and/or bronze (13.7%), ductile iron (12.3%), gray iron (13.7%), steel (24%), and other metals (e.g., magnesium, zinc, stainless steel; 13.7%). This not only attests to the range of viewpoints represented in the survey, but also sufficiently matches the proportionality of different metals in the breadth of U.S. metalcasting.

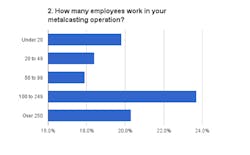

Similarly, our survey respondents are representative of the range of plant sizes — see Chart No. 2 — for U.S. metalcasters. Just fewer than 20% of all respondents (19.8%) represent businesses with fewer than 20 employees; 18.4% represent businesses with 20 to 49 workers; 17.9% of respondents’ firms have 50 to 99 employees; 23.76% are with firms that have 100 to 249 workers; and 20.3% are affiliated with metalcasters that have over 250 employees.

Current Performance, Future Results

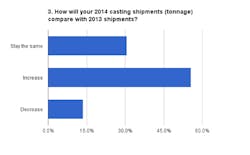

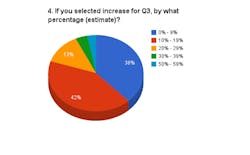

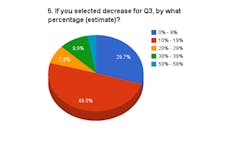

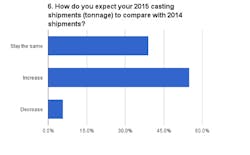

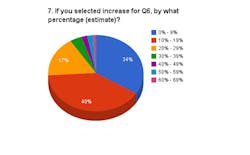

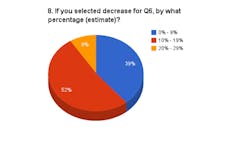

We asked all respondents to assess their current business performance — see Chart No. 3 — in respect to shipped volume of castings during 2014, compared to the results of 2013. We also asked for estimates of the rate of increase or decrease — see Charts No. 4 and 5, wherein we see that most of the respondents in each case expect the change will be less than 20% from last year’s result.

The most positive assessment of the current year belongs to the gray iron foundry respondents, 66% of whom anticipated higher shipment levels for the current year than for 2013. Steel foundries (59%), ductile iron foundries (58%), and aluminum metalcasters (55%) also show confidence about 2014’s results. Among the brass/bronze-producing respondents, positive expectations are restricted to just 41% of the total.

The positive views of the current year also seems to favor midsized and larger metalcasting operations: 73% of the operations with 20-49 workers anticipate better results this year than during 2013, as did 67% of the operations with over 250 workers, and 59% of respondents with 100 to 249 workers. The other segments are less hopeful: just 43% of the respondents from operations with 50 to 99 workers, and 36% of respondents from plants with 20 or fewer workers, expect this year to increase their tonnages of shipments.

These results also suggest economic progress over the findings of our 2014 Outlook survey. Twelve months ago, we reported a nearly even split (33.5%/30.4%/36.0%) among respondents’ assessments of the then current year’s (2013) results, with a slight majority confirming performances that lagged the previous year’s (2012) result. A larger number (54%) expressed confidence for better expansion in 2014.

Moreover, those results in 2013 were sustained regardless of sorting according to metals cast or plant employment total. If there is a trend, it favors the current year, is moving in the positive direction.

Returning to the current survey — see Chart No. 6 — 55.6% of all respondents indicated 2015 will show improvement over the current year, and 30.7% indicated the current year would be even with 2014, in terms of tons of castings shipped. Those expecting improved levels of shipments — see Chart No. 7 — see all manner of possible growth scenarios, from marginal to magnificent. Just 13.7% of all respondents expect to record diminished volumes of shipments next year — see Chart No. 8 — and more than 50% anticipate that decrease to in the range of 10-19% of the current year’s shipment volume.

The most positive views of the next year are to be found among gray iron casting producers, 69% of whom forecast that tonnages shipped this year will increase; 59% of aluminum casting producers, 54% of ductile iron casting producers, and 51% of steel casting producers also expect increases.

However, among brass/bronze casting producers, only 41% of respondents expect to record increased shipments in 2014.

The respondents’ forecasts for 2015 show more enthusiasm among the cohort for plants with 20 to 49 employees: 70% of them expect the coming year to feature higher shipment volumes. Their optimism is shared by 60% of respondents from plants with over 250 workers; 59% of respondents from sites with 100 to 249 workers; and 53% of those from plants with 50 to 99 workers. There is less optimism among the respondents of smaller metalcasting operations: just 32% of the respondents representing plants with 20 or fewer employees anticipate higher shipment volumes in 2015 than during 2014, and 59% of that segment anticipate no change from this year to next.

Affecting Investments

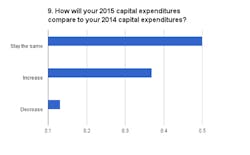

These analyses matter as a guide to metalcasters’ capital investment plans for 2015 — see Chart No. 9. Among all respondents, 50.0% intend to maintain the same value of capital investments from this year to next year; 36.9% of all respondents intend to increase the value of their capital investments in 2015. Decreasing capital investment totals may be in the plans of 13.1% of respondents.

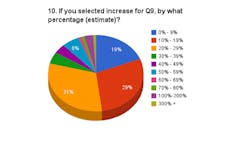

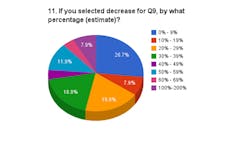

The 70% of respondents who indicated intentions to increase capital spending in 2015 — see Chart No. 10 — seem to be inclined for steady progress, with increases of 30% or less above the current year’s investments. The 25% who will be reducing capital spending in 2015— see Chart No. 11 (5% declined to indicate) — are more varied in their estimates.

The ductile iron foundries (42%) show the greatest inclination to increase their capital spending in 2015; the other metalcasters (brass/bronze, 38%; steel, 37%; aluminum, 34%; gray iron, 32%) are all within hailing distance of the front-runner.

In terms of the plant size, smaller metalcasters appear the most eager to invest in 2015: 50% of plants with 20 to 49 workers will be raising capital outlays, and 42% more will be maintaining their current investment levels. Foundries/diecasters with 20 or fewer workers indicate a strong likelihood (62%) of maintaining the 2014 capital investment levels, with another 26% set to increase the current level.

In fact, metalcasting plants regardless of size are unlikely to reduce their investment next year, the highest probability being among those plants with 50 to 99 workers; 19% of them will be cutting back capital spending in 2015.

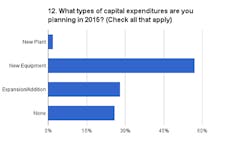

The targets of their investments — see Chart No. 12 — are most likely to be new production equipment or systems; 57.3% of respondents indicate such investment plans. A small but noteworthy percentage, 2%, intend to invest in new plants in 2015, while 28.1% of all respondents will be expanding their existing production capabilities.

At the same time, it’s worth recognizing that more than a quarter of all survey respondents, 26.1%, have no capital spending plans to report for 2015.

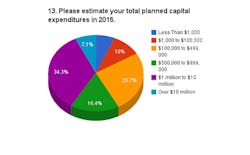

The range of values in respondents’ capital investment programs — see Chart No. 13 — is instructive: 6.4% will invest less than $100,000 in total; 7.1% who will invest $100,000-$499,000; 25% will invest $100,000-$499,000; 15.7% will invest $500,000-$999,000; 33.6% will invest $1 million to $10 million; and 7% will invest over $10 million.

The capital for these plans will be borrowed, in most cases, though only 8.9% of all respondents indicate plans to increase their borrowing level. Contrarily, 35.6% report no current debt, and 10.4% of respondents indicate they will be retiring their debt total in 2015. The remainder – those that intend to maintain their current debt levels – comprise 45.0% of all respondents.

With generally positive expectations for the coming year’s business prospects, and a confident approach to financing growth, studying the plans for coming investments will reveal much about the emerging state of metalcasting technology in 2015.

Read the third and final installment of this series, Metalcasting Business Outlook 2015: Forward Progress.