Metalcasting Business Outlook 2015: Forward Progress

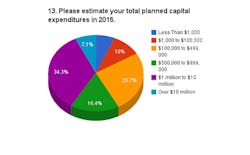

One reliable indicator of business confidence is capital spending programs, and metalcasters’ forward thinking on that basis is instructive: while more than 86% of all survey respondents expressed confidence that their production volumes in 2015 would equal or exceed this year’s totals, roughly 74% of respondents — see Chart 13— plan capital investments that will support their business programs.

This is the third installment of a series. Read part 1, The Metalcasting Business Outlook 2015 and part 2, Present Results, Future Prospects.

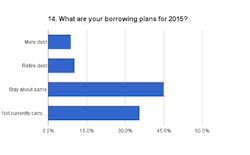

In general, survey respondents aim to execute their capital programs within their current credit arrangements, as fewer than 10% of the total indicate plans for new debt issuance — see Chart 14 — and slightly more than that aim to retire debt during 2014.

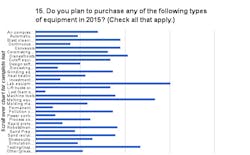

The specific nature of metalcasters’ investment plans — see Chart 15— also offer insights to the nature of the industry today, its priorities and its objectives. For example, 30.2% of all respondents in this multiple-selection question noted their intention to invest in new Laboratory Equipment. This is refers mainly to metallographic technologies used to inspect and test the product quality – mainly for product quality testing and qualification. A similar category ranks third on the long list, Testing/Inspection Systems (23.5%), a catch-all indicating non-destructive testing systems (spectrography, tensile testing, etc.) as well as more functional equipment, like radiography and laser-based three-dimensional measuring devices.

The second-ranking selection among all respondents, Melting Equipment, was identified by 26.8% of respondents, suggesting metalcasters’ expectations of sustained consumer demand for cast products.

A desire for smoother or more reliable plant processes is indicated by several top-ranking selections. 20.7% of respondents plan to invest in Cranes and/or Hoists; 19.0% plan to invest in Conveyors; and 18.4% plan to invest in Robots and/or Manipulators.

There is a similar consensus among respondents interested in finishing cast products: 19.0% intend to invest in Blast Cleaning Equipment; 17.9% will invest in new Machine Tools; and 17.3% will invest in new Grinding Equipment.

Filling out the top-ranks of capital investment targets is a evidence of foundries need to update and/or modernize their most characteristic operations — 17.9% of respondents indicate they will invest in Sand Reclamation Equipment — and the need for metalcasters broadly speaking to operate within regulatory standards: 17.3% of respondents will invest in Pollution Controls.

Managers’ Dilemmas

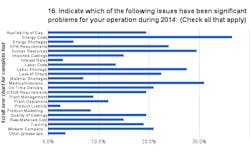

We need not rely on investment plans to know what issues concern metalcasting decision-makers. Survey respondents provided a view of their concerns over the past year — see Chart 16—leading with Energy Costs (36.5%.) Medical/Insurance Costs (31.0%) followed among respondents’ concerns in the current year, and then Human Resources (29.5%) and Labor Shortages (27.5%). (As in the previous question, this series allowed respondents to select multiple options, so the total response rate exceeds 100%.)

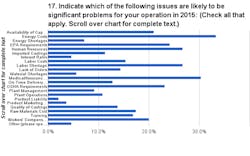

Looking forward, a similar range of issues are cited by respondents as their top concerns for 2015— see Chart 17—including again Energy Costs, for 33.3% of all respondents; Medical/Insurance Costs (30.3%), and a tie among Human Resources (26.7%) and Labor Shortages (26.7%).

Regulatory issues are on the horizon for a significant number of respondents: EPA Requirements (24.1%) and OSHA Requirements (23.1%) loom as the fifth- and sixth-ranking concerns, followed by two specific financial matters: the Availability of Capital (21.0%) is cited as the seventh ranking concern; Workers’ Compensation (20.0%) and Raw Materials Costs (17.4%.)

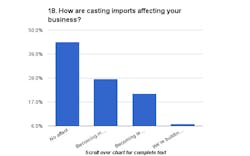

The challenge of global economics has been a standing concern for North American manufacturing for decades, prompting us to inquire of survey respondents how casting imports affect their business conditions — see Chart 18. While there is no majority opinion, it is perhaps surprising to note that 44.6% of all respondents indicate imports have no effect on their business, 20.8% responded that imports are becoming less of a competitive factor.

The reasons for these results are as varied the respondents, but among the detailed responses we collected on this point, the trends favoring domestic sourcing include product design and selection (“As we manufacture very small quantities of special product, we have no import competitors”) and product quality (“Some customers will pay the higher price for higher quality castings."); as well as the re-shoring phenomenon that has influenced many businesses in the past three years (“Castings outsource in previous years have returned as the benefits are outweighed by the hidden costs associated with offshoring.")

At the same time, the standard challenge presented by off-shore suppliers apparently remains in some product segments (“It is difficult to compete with imported castings produced by lower labor costs abroad,” a respondent affirmed.)

Productivity and Personnel

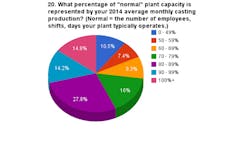

In the final phase of the survey we asked respondents to characterize the strength and potential for growth at their particular businesses. Using operating capacity as a gauge — see Chart 20 — we asked each respondent to compare his or her average monthly output to the plant’s nominal capacity. The results, which do not account for regional, product, or process diversity, nevertheless depict a metalcasting industry that has an ability to increase its productivity. Among all respondents, 6.3% are operating at less than 40% capacity; 18.9% are operating at 41-70% capacity; 45.3% are operating at 71-90% capacity; 15.1% are operating at 91-100% of capacity; and 13.8% report they are currently operating at above their operation’s designed capacity.

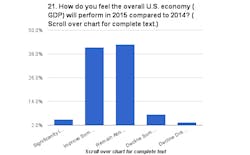

Turning this line of inquiry around, we asked respondents to project their expectations for U.S. economic growth (GDP) — see Chart 22 — and while there is no clear consensus there is little confidence for significant improvement. Rather, the largest cohort of respondents (42.8%) expect little change in U.S. economic conditions, and slightly fewer (41.3%) believe GDP will “improve somewhat.”

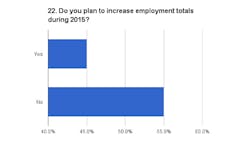

The matter of employment levels is a perennial live wire: cutting employment may precede downsizing plans, or it many indicate marginal cost savings. Adding employment may indicate business expansion, or it may suggest catching up to past oversights. As 2015 approaches metalcasters are not overly inclined to add new employees — see Chart 22 — though the split is not as wide as generally perceived.

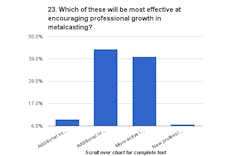

A related issue is the availability of suitably skilled employees, indeed of qualified individuals for work in the management of metalcasting operations — see Chart 23. We asked respondents to rank prospects for improving the pool of qualified metalcasting industry employees, and their preferred solution involves new or alternative training opportunities with colleges and or vocational schools (43.8%), as well as more direct involvement of metalcasters with trade associations and colleges (40.1%) to prepare students for specific industrial skills. Many fewer respondents saw value in developing new academic training programs, or in launching new professional organizations to foster or confer such training.

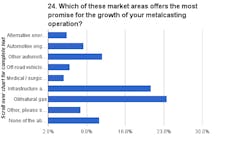

Finally, we asked respondents to help identify the prospects of consumer markets for cast products — see Chart 24. The outright favorite selection is the Oil/Natural Gas market segment, which 23.6% cited. Construction Markets came close (20%), as did Other (Non-Engine) Automotive Components (11.8%), and then Automotive Engines (11.3%). The ranking also includes “None of the Above,” suggesting there may be other possibilities or applications for cast metal products.

Undoubtedly, there are other applications for castings, and those remain among the many outcomes to be revealed during 2015.