Demand for Lightweight Auto Parts Rising +5% Annually

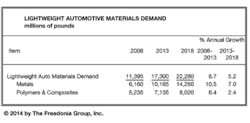

North American automakers’ demand for lightweight materials is forecast to rise 5.2% annually to a total of 22.3 billion pounds (11.15 million tons) in 2018. The conclusion is found in a five-year market study made available by The Freedonia Group. Analyst Bridget McMurtrie observed that “advances will significantly outpace gains in automotive materials overall.”

McMurtrie added that “Regulatory pressure will be the major force propelling growth.”

The drive for lighter automotive designs is based largely on increasingly strict fuel economy standards promulgated by the U.S. Environmental Protection Agency, and thus automakers’ determination to reduce vehicle weights. Ford Motor Co.’s introduction of an

The best growth prospects for lighter materials are forecast for exterior and structural components, the Freedonia study notes. Continuing development of lightweight materials suitable for use in structural applications and the weight savings such materials may provide, are encouraging designers to re-examine such prospects. Exterior and structural parts will account for nearly 75% of total average vehicle weight reduction through 2023, Freedonia determined, with body and frame applications accounting for about 50%.

Lightweight designs for interior applications are “relatively mature” and will see only limited growth going forward, according to the study. It observed that plastics have already been established in designs for automotive interior components, so opportunities for further weight reduction are limited.

Aluminum and high-strength steel are forecast to be the primary lightweight materials gaining presence in automotive design. In particular, Freedonia sees aluminum gaining use in exterior and structural applications (e.g., the 2015 Ford F-150), as automakers renew their consideration of weight and strength factors for automotive closures and panels.

Furthermore, the group ventures that other automakers will study Ford’s switch to aluminum for automotive body design to determine the value and viability of similar conversions.

However, high-strength steel is predicted to have the best growth opportunities for automotive structural and framing applications because of its relatively low cost and continuing development of new grades that combine material strength and formability.

Engineered plastics will remain the top polymer material through the forecast period, having already replaced metals in several applications based its design flexibility.

Demand for high-performance composites will increase rapidly from a currently low level due to the materials’ substantial vehicle weight savings potential, although cost will remain a barrier to widespread applications.

Lightweight Automotive Materials in North America is a 375-page report available for purchase from The Freedonia Group. Contact the group by phone (440-684-9600) or e-mail, or visit www.freedoniagroup.com.

About the Author

Robert Brooks

Content Director

Robert Brooks has been a business-to-business reporter, writer, editor, and columnist for more than 20 years, specializing in the primary metal and basic manufacturing industries. His work has covered a wide range of topics, including process technology, resource development, material selection, product design, workforce development, and industrial market strategies, among others.